Outcomes of the European Council meeting on 21-22 March

EU leaders met in Brussels on Thursday 21 March and Friday 22 March. On the first day of the summit, EU leaders adopted conclusions on Ukraine, security and defence, the Middle East, enlargement and reforms, migration, preparedness and crisis response and the European Semester. The conclusions reiterate the EU’s determination to continue to provide Ukraine and its people with all of the necessary political, financial, economic, humanitarian, military and diplomatic support for as long as it takes. The conclusions also stress that the EU and its Member States should accelerate and intensify the delivery of all of the necessary military assistance, including the procurement of ammunition for Ukraine. Concerning the Middle East, the EU leaders expressed their deep concern about the catastrophic humanitarian situation in Gaza. They called for an immediate humanitarian pause leading to a sustainable ceasefire, the unconditional release of all hostages and the provision of humanitarian assistance, and urged the Israeli government to refrain from carrying out a ground operation in Rafah, where over one million Palestinians are seeking safety. Finally, they gave their green light to open accession negotiations with Bosnia and Herzegovina. On the second day, the leaders discussed external relations and agriculture.

European Commission addresses unanimity voting in taxation in enlargement communication

The European Commission raised the possibility of moving from unanimity to qualified majority voting (QMV) on tax and other matters as part of a communication on pre-enlargement reforms and policy reviews published on Wednesday 20 March. As Albania, Bosnia and Herzegovina, Georgia, Moldova, Montenegro, North Macedonia, Serbia, Turkey, and Ukraine hold EU candidate status, the communication looks at the implications of a larger EU in four main areas: values, policies, budget and governance. “Questions around the EU’s capacity to act exist already in a Union of 27 Member States. This concerns in particular unanimity voting rules in the Council. While most decisions are now taken by qualified majority in the Council, in some areas, decisions need to be taken by unanimity in the Council, as is the case for tax, foreign policy and certain social matters. In a larger Union, unanimity will be even more difficult to reach, with increased risks of decisions being blocked by a single Member State”, the European Commission wrote. The communication recalls that the EU Treaties already foresee so-called “passerelle clauses” allowing for a shift from unanimity to qualified majority voting within the Council in key areas, which have to be activated with a unanimous decision either from the Council of the European Union or the European Council. Acknowledging the resistance from some Member States who fear becoming isolated on matters of essential strategic national interest, the European Commission said that a possible way forward could be to combine the activation of the “passerelle clauses” with appropriate safeguards, such as European Council conclusions providing for the possibility for one or several Member States to invoke exceptional national interest grounds to continue discussions to reach a satisfactory solution, or to seize the European Council to deliberate on the matter. The Commission said it will carry out the pre-enlargement policy reviews in early 2025 and will make substantive reform proposals in individual sectors.

European Commission issues economic brief on growth-friendly taxation in a high-inflation environment

The European Commission’s Directorate General for Economic and Financial Affairs published on Wednesday 20 March an economic brief focusing on challenges and possible solutions related to recurrent immovable property and labour taxation during periods of high inflation. Recurrent property taxes are among the taxes least detrimental to growth, the authors argued. If they are based on property values, then regular updates of the tax base are required to maintain their revenue potential and economic efficiency as well as the equal treatment of taxpayers. At the same time, the update of property values could lead to sudden and large upward revisions in tax liabilities when inflation is high, which may increase resistance against reforms aimed at shifting taxation towards immovable property. In the authors’ opinion, practices aimed at increasing the frequency and reducing the cost of updating property values and temporary tax reliefs on property taxes can help overcome such increased resistance. Resistance can also be linked to liquidity issues for the non-negligible number of taxpayers that own property but have relatively low incomes. Resistance in these cases could be dealt with by the possibility of tax deferrals or by targeted and means-tested tax relief for low-income households, according to the paper. The design of labour taxation for low-wage earners is also important to support inclusive growth, as workers with low incomes react more sensitively to work incentives at the extensive margin (i.e. the decision to work or not), the authors found.

Pascal Saint-Amans recommends broader external border taxes as new resources for the EU budget

In a policy brief published on Thursday 21 March Pascal Saint-Amans, former Director of the Centre for Tax Policy and Administration (CTPA) of the OECD and non-resident fellow at the think tank Bruegel, examined the 2023 revised package of new own resources proposals for the EU budget and proposed new ideas, including exploring external border taxes. “Failure to move forward would jeopardise the ability of the EU to keep funding its existing projects, especially at a time when interest rate increases will make the repayment of both capital and interest heavier”, Mr Saint-Amans wrote. In his view the 2023 revised package is “pragmatic and moves in the right direction but does not go far enough”. Mr Saint-Amans particularly welcomed the fact that the Commission did not go back to the idea of a European digital services tax (DST) as a substitute for the OECD deal. Beyond the urgent need to agree on this package, the debate about own resources should focus, in his view, on whether the EU will be able to build genuine own resources based on common tax policies. In this regard, the 15 percent global minimum tax could have offered an opportunity to mutualise some resources at the EU level as a genuine own resource, he said. While the prospect of new own resources deriving from harmonised taxes remains unlikely due to the unanimity requirement to decide on tax matters, he recommended exploring how other external tax borders of the EU could be a way to move towards genuine new own resources. For instance, in the area of personal income tax, establishing a common exit tax on EU countries’ residents moving abroad to avoid paying capital gain taxes could serve the purpose of protecting EU countries’ tax bases and developing a new own resource, he said. This could also be considered in the field of wealth taxation or inheritance duties. Rather than harmonising taxes, which proves difficult, focusing on protecting the revenues of EU members by common borders may unleash some potential, Mr Saint-Amans concluded.

New OECD working paper on the design of presumptive tax regimes in selected countries

On Tuesday 19 March, the OECD published a new working paper compiling information on the presumptive tax regimes existing in a selection of OECD and non-OECD countries (Argentina, Brazil, Colombia, Costa Rica, France, Hungary, Italy, Mexico, South Africa, Tunisia, Uruguay). Presumptive tax regimes (also known as simplified tax regimes) aim at encouraging tax compliance and business formalisation by reducing tax compliance costs and by levying lower tax rates as compared to the standard tax system. These regimes usually target micro and small businesses and levy tax on a presumed tax base that intends to approximate taxable income by indirect means. They can be particularly relevant where actual taxable income is difficult or costly to assess accurately. The paper identifies common practices adopted across the countries examined and provides multiple examples of best practices observed in these regimes. The paper also highlights the main challenges generally observed in the presumptive tax regimes under study, which might undermine the role of these regimes in incentivising business formalisation and strengthening tax compliance over time. The optimal design and administration of a presumptive tax regime requires a regular and evidence-based evaluation to verify the regime’s coherence and whether its objectives have been fulfilled, the authors argue. Presumptive tax regimes require further attention from tax policy makers and tax administrations, the OECD concludes.

David Bradbury to step down as Deputy Director of the OECD CTPA

The Deputy Director of the OECD Centre for Tax Policy and Administration (CTPA), David Bradbury, announced on Monday 18 March in a LinkedIn post that he is leaving his position after nearly 10 years within the organisation for personal reasons and returning to Australia. Mr Bradbury was appointed deputy director of the CTPA in April 2023, when Manal Corwin became Director of the CTPA. Mr Bradbury played an instrumental role with the delivery of the OECD/G20 BEPS Project in 2015, the pivotal 2018 Interim Report of the Task Force on the Digital Economy and the landmark 2021 international tax agreement, which has been agreed by more than 140 jurisdictions and has delivered the global minimum tax that came into effect on 1 January 2024. “For the next three months, I remain committed to continuing my service to the OECD. Beyond that, I am excited by the prospect of taking on new challenges, and I am approaching the next steps in my career with an open mind and a continuing desire to make a contribution”, David Bradbury wrote.

ETAF annual report 2023

The European Tax Adviser Federation (ETAF) published on Monday 18 March its annual report presenting its main activities in 2023. In this edition, we put the spotlight on our work on the Anti-Money Laundering package, the rationalisation of EU tax reporting requirements, the VAT in the digital age package, DAC8, the proposal for a Head Office Tax system for SMEs (HOT), the Business in Europe: Framework for Taxation (BEFIT) proposal, the new proposed framework for “Faster and Safer Relief of Excess Withholding Taxes” (FASTER) and the Transfer Pricing Directive proposal. 2023 was also an eventful year, with two ETAF conferences, our participation in the EU Tax Symposium and the EU Tax Observatory’s annual conferences, our members congresses as well as several meetings with tax officials and stakeholders. “Looking ahead to 2024, a pivotal year marked by the EU elections, ETAF remains committed to advocate for balanced and fair tax rules, to support modernizing the international tax system, and to champion strong, independent and regulated tax professions across Europe”, ETAF President Philippe Arraou said in the foreword.

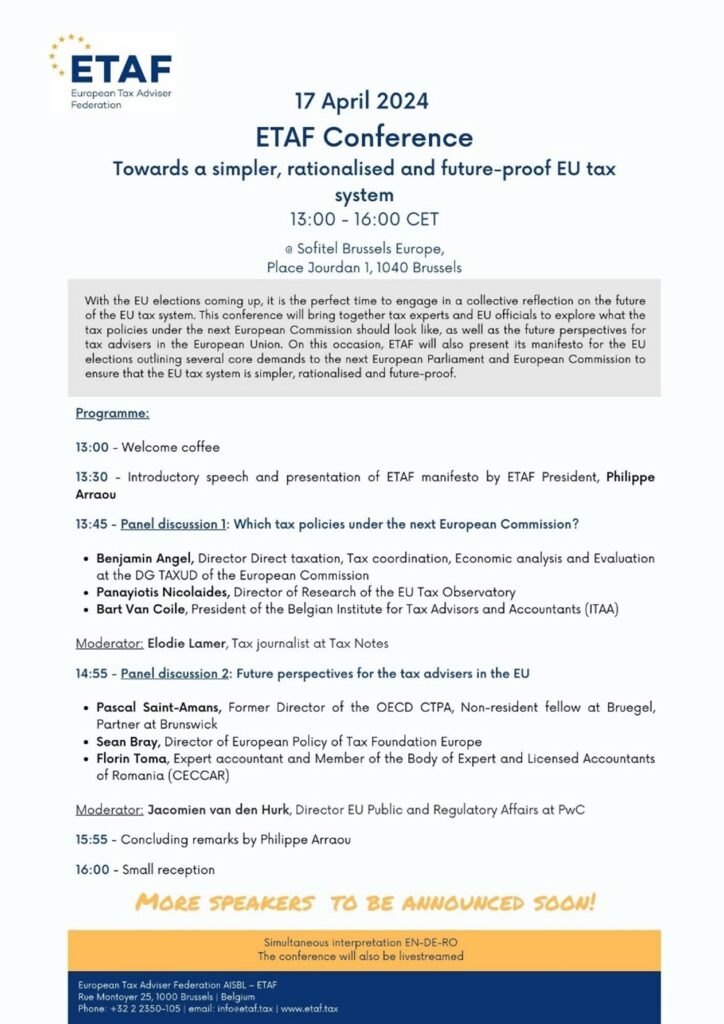

ETAF Conference on 17 April 2024: registration opens!

Register here: https://sweapevent.com/etafconference17april2024